CRUSHED – BUT NOT BROKEN

IBW is the engine. Nebari is the backstop. Aznalcóllar is the upside kicker.

The macro tape is still being driven by war headlines, oil and shifting rate expectations. Reuters reported on March 19 that the Iran conflict had clouded the Fed path, with the Fed holding rates steady and sticking to just one projected cut in 2026 as oil complicated the inflation outlook. Reuters then reported today that oil dropped sharply and stocks jumped after Trump postponed planned strikes on Iranian power plants for five days. That is the backdrop: still volatile, still headline-driven, and still not a clean risk-on tape.

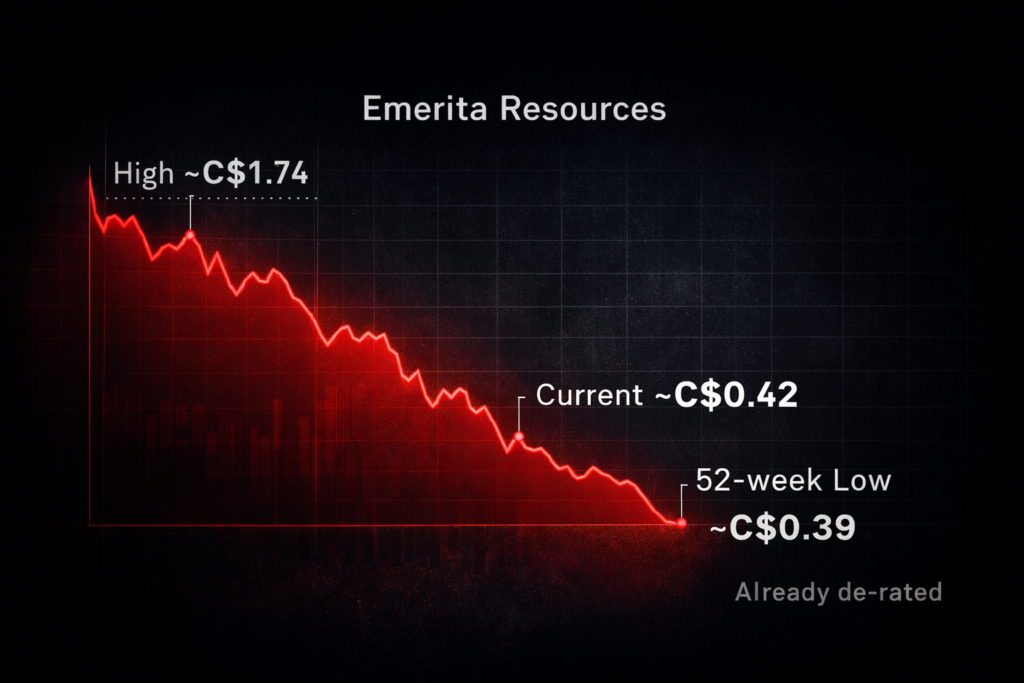

TL;DR: EMO is trading around C$0.42, just above its 52-week low near C$0.39 and far below its C$1.74 high. On the current share count, that is roughly a C$121.6 million market cap; using September 30 cash and debt, it works out to a rough enterprise value of about C$104.3 million. Against that, the company has a 25.76 Mt IBW resource, an updated MRE expected in the coming months, a PFS targeted for the end of Q2 2026, advancing permitting, C$27.2 million of cash at September 30, management saying it is well-capitalized after a C$26 million equity financing, and up to US$50 million of Nebari credit capacity.

The kind of stock that starts to matter in ugly markets

In compressed markets, one of the clearest tells is relative behavior. The better setups are often the names that have already been hit hard, are sitting near their lows, and stop behaving like fresh liquidation candidates. EMO increasingly fits that mold. From March 11 to March 23, EMO fell 14.0%, almost identical to the TSX Venture’s 14.0% slide over the same stretch. For a stock already trading just above its 52-week low, that is an encouraging signal: the market is no longer treating it like a unique problem child. It is mostly moving with the tape. That is often how a coiled spring starts to form in juniors. This is an inference from the price action, not a guarantee.

There is a simple reason that matters here. EMO has already done a lot of its de-rating. Reuters/LSEG shows the stock’s 52-week range at roughly C$0.39 to C$1.74, and Emerita’s own site shows it around C$0.42 today. In other words, the market has already taken a sledgehammer to the valuation. That does not make it immune if the macro gets worse. It does mean the stock no longer needs heroic sentiment to work from here. It just needs the market to stop treating every small-cap resource name as if it were still in free fall.

Nebari is the backstop

The cleanest part of the EMO setup is that it is not resting on retail enthusiasm. It already has a specialist lender underneath it. In August 2024, Emerita put in place a Nebari facility for up to US$15 million, priced at Term SOFR plus 11.5% with a 4% floor, which implies a minimum coupon of roughly 15.5%. In September 2025, that facility was expanded with a US$35 million standby fourth tranche, taking total capacity to US$50 million. Crucially, Emerita said only Tranche 1 had been drawn, while Tranches 2, 3 and 4 remained at the company’s discretion. That is not a distressed borrower maxing out the card. That is a staged capital structure being built around a project that is still moving up the value curve.

The security package is what turns this from a financing headline into a valuation tell. Emerita’s 2025 audited financials say that upon receipt of an exploitation concession, Nebari is entitled to a first-lien senior security over IBW’s future tangible and intangible assets, plus a first-priority mortgage and security interest over the project’s mining claims, concessions, permits and related property. In December, after the TSXV approved the upsizing, Nebari waived the extra warrants tied to the larger facility and said IBW was well positioned to move toward execution, citing growing resources, modest expected capital cost, established infrastructure and a supportive mining jurisdiction. That does not mean Nebari has published a current NPV. It does mean that a serious credit fund has already built a senior, asset-backed funding lane under IBW. In this tape, that matters.

That is the part worth emphasizing. Nebari is not there to dream. Nebari is there to get repaid first. The read-through is straightforward: IBW has already reached the point where specialist capital is willing to underwrite downside against it, and willing to expand that capacity as the asset de-risks. In weak markets, that kind of backstop is worth more than promotion and more than in-situ screenshots.

TL;DR: Nebari does not prove a final NPV. It does prove that IBW is already being treated as financeable collateral rather than as a pure exploration story.

IBW is the engine

The base case is still IBW, and IBW is already substantial. Emerita’s April 2025 NI 43-101 technical report shows 18.96 Mt indicated at 8.44% ZnEq and 6.80 Mt inferred at 8.72% ZnEq, based on 105,554 metres of drilling across 299 holes. The resource spans La Romanera, La Infanta and El Cura, and all three deposits remain open for expansion. That is already a real inventory, not a one-hole story.

The 2026 catalyst stack is also unusually tangible for a stock trading around a C$120 million market cap. In January, the company said it expects an updated MRE in the coming months, the PFS is scheduled for completion by the end of Q2 2026, and the public-comment period for permitting is expected in Q1 2026, to be followed by the Unified Environmental Authorization. The PFS, which was awarded to SLR in December, is expected to cover mine-to-mill design, process-plant and flowsheet design, surface infrastructure, capital and operating costs, and financial analysis. That is when the market stops arguing about “potential” and starts valuing a project.

The underlying data set is still getting better ahead of that study. In February, Emerita said assay results from 91 holes had been prepared for the updated MRE that will feed the PFS, versus 39 holes in the 2025 El Cura maiden MRE, with drilling continuing at El Cura and La Infanta to convert more inferred material into higher-confidence categories. That is not cosmetic progress. That is exactly the sort of quiet de-risking that can change mine shape, categories and study quality.

Metallurgy is also moving in the right direction. In May 2025, Emerita reported 81.5% gold recovery for La Romanera in updated CLEVR testing, an improvement over the recovery assumptions used in the March 2025 MRE. Then, in March 2026, it reported Albion-route results of 81% gold recovery and 96% silver recovery from post-flotation material, while noting that the final flowsheet will be selected as the PFS advances. That is important because better recoveries are not cosmetic; they go straight into value capture. A resource can be large and high grade, but the money is made in the plant. On that front, IBW keeps improving before the study is even finished.

This is why the IBW story looks increasingly difficult to ignore. The project now has scale, a live study cycle, improving metallurgy, advancing permits and a lender already positioned behind it. That is not what an early exploration story looks like. That is what a junior looks like when it is starting to cross into the mine-development lane.

Aznalcóllar is still the upside kicker

Aznalcóllar still matters, but it should be treated as optional upside rather than something required to make the stock work. Emerita said in December that its objective remains to acquire the right to develop the Aznalcóllar project and that the administrative court, not a criminal appeal, is the path that matters. In January, the company reiterated that the legal dispute is expected to be resolved in the coming months. That means the optionality is still very much alive.

Just as importantly, the company’s own year-end MD&A keeps the analysis honest. It repeats the often-cited historical Aznalcóllar tonnage figures, including the 20 million tonne higher-grade portion from the previous operator, but explicitly says a qualified person has not classified that estimate as a current resource or reserve and that it should not be relied upon. That actually makes the overall setup cleaner, not worse. It means the base case does not need AZN padding. If the administrative ruling lands in Emerita’s favor, shareholders get a meaningful second leg of upside on top of IBW. If it does not, the core case still sits on a real project.

The setup from here

The numbers are what make the setup compelling. At roughly C$0.42 and 289.46 million shares outstanding, EMO is about a C$121.6 million market-cap story and a rough C$104.3 million enterprise-value story using the September 30 balance sheet. Against that, the company had C$27.24 million of cash at year-end, said it had sufficient working capital for the next twelve months, and said in January that it was well-capitalized after a C$26 million equity financing and a US$50 million credit facility. That is a lot of balance-sheet support for a junior in a stressed market.

The cleaner posture is accumulation, not maximum aggression. The macro backdrop is still too event-driven for all-in positioning, and the whole point of this tape is that oil and war headlines can still move everything at once. But that does not diminish the setup. It sharpens it. When markets are compressing, the names worth circling are the ones that are already heavily de-rated, have stopped acting like broken stories, and still have hard assets, hard capital and live catalysts underneath them. EMO increasingly fits that description.

As an investor for many years I fear the leverage of the corrupt , hidden agenda of the political arena with Mexico! Nothing is sacred with these people! Nothing is secure! Look at history!

If ANZ becomes an asset of Emerita the market cap including IBW will be a little north of 3 Billion CDN by years end.

Emerita will be an interesting play considering it’s current market cap valuation @ 122 Million CDN.